Written by Blake Blackburn

The multi-family investment market in the Central Valley has slowed significantly from its peak just a few years ago. This year has seen only 47 transactions, 56% fewer than the 107 transactions recorded during the same period in 2018.

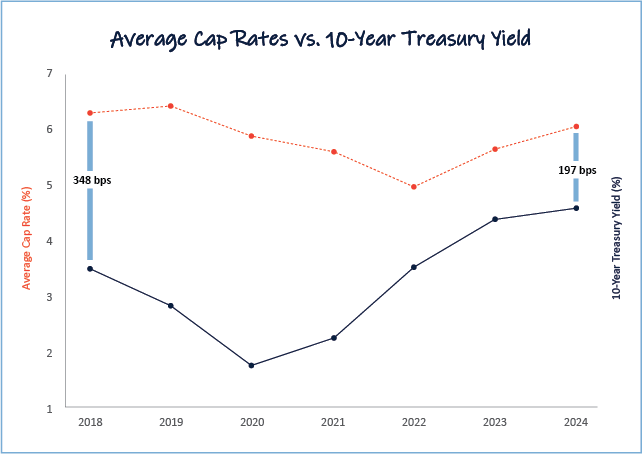

Despite the sharp decline in deal velocity, average capitalization [CAP] rates today are very similar to those in 2018: 6% in the first three quarters of this year compared to 6.26% in 2018.

Treasury yield, market dynamics

A significant rise in the 10-year Treasury yield has reshaped the investment landscape. The median yield increased from 2.78% in 2018 to 4.03% in

2024—a 125 basis point jump. This has compressed the spread between CAP rates and Treasury yields, reducing transaction activity.

Delta in CAP rates, treasury yields

The spread between CAP rates and Treasury yields shrank from 348 basis points in 2018 to 197 basis points in 2024, a 151 basis point reduction. This has two key impacts:

- Loan-to-Value Ratios: A smaller spread leads banks to tighten lending, offering lower loan-to-value ratios and requiring investors to put down more cash, thus limiting buyer activity.

- Investor Returns and Leverage: Wider spreads help preserve returns when using debt and can even create positive leverage, where returns increase through the strategic use of debt. However, the reduces spread in 2024 has made debt financing less appealing for investors.

Blake Blackburn is a multi-family investment advisor with Visintainer Group in Fresno.

Related Posts

-

Fresno’s home of the viral Anaconda Burrito is expanding near River Park Posted: March 12, 2026 at 3:19 pm

Fresno’s home of the viral Anaconda Burrito is expanding near River Park Posted: March 12, 2026 at 3:19 pmFresno’s Taqueria Yarelis, which achieved viral fame for its giant

Read more » -

Fresno massage studio among nation’s highest-rated women-owned businesses Posted: at 1:49 pm

Fresno massage studio among nation’s highest-rated women-owned businesses Posted: at 1:49 pmA Fresno business owner's massage studio was recently ranked as

Read more » -

Long lines lead to storefront as Tacos El Cabezon opens Downtown Fresno location Posted: at 12:21 pm

Long lines lead to storefront as Tacos El Cabezon opens Downtown Fresno location Posted: at 12:21 pmTacos El Cabezon, one of Fresno’s most talked-about taco destinations,

Read more » -

Fresno has what AI needs. Getting investors to notice is another story Posted: at 11:28 am

Fresno has what AI needs. Getting investors to notice is another story Posted: at 11:28 amA new study suggests that the Central Valley and areas

Read more »

Central Valley Biz Blogs

-

BLOG: For the Central Valley, policy must work in practice — not just on paper

Posted: at 12:40 pm

For the Central Valley, Sacramento is not abstract. State policy

Read more » -

BLOG: California’s tribal casinos trample smaller cardrooms with new regulations

Posted: March 11, 2026 at 9:18 am

While writing a book about California politics a quarter-century ago, I devoted

Read more »